Having trouble with the life insurance conversation?

If you are like many financial advisors you spend much of your time focused on helping clients build wealth for important goals while minimizing portfolio risks. Unfortunately, too few spend time addressing non-portfolio risks that can prevent clients from reaching those goals. When you do this, you’re missing an aspect of risk management that can affect both your clients’ financial well-being AND your own. Fortunately, DBS has taken the guesswork out of it and have a tool that will help you determine how much – and what type – of life insurance your clients need!

Specifically, as clients age one of three things will likely happen: they’ll die too soon, get sick along the way, or live too long. The key is to protect clients at every stage, no matter what unknowns might affect their financial situation.

Transitioning to the Life Insurance Topic

Many financial advisors don’t bring up the life insurance conversation because of the concern of the unknown. . . not knowing how much coverage or the type of coverage is appropriate for the client. Even transitioning into a conversation about like insurance may be uncomfortable.

If you are an advisor that has been having the portfolio risk discussion with your clients and you want to have the life insurance discussion consider the following transition: “Up until this point, most of our conversation has been focused on minimizing portfolio risks to help you reach specific financial goals. So, we’ve talked about things like diversification and asset allocation. However, I want to spend a little time addressing risks that can prevent you from reaching those goals.

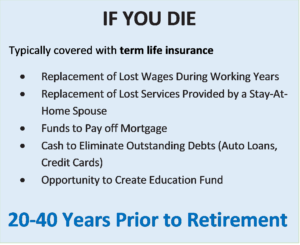

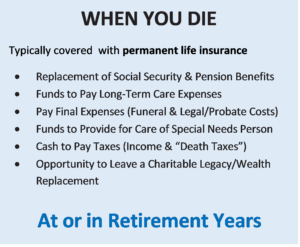

As you age, one of three things will likely happen: you’ll die too soon, get sick along the way, or live too long. Insurance is key to protecting yourself and important family goals, at each of these stages. To help me generally determine the types of life insurance you may need I just need to ask you, do you want your life insurance to provide protection if you die or when you die?

Specifically, term insurance is typically purchased protect your family if you die prematurely and want to provide protection for things such as (read below). However, some form of permanent coverage is typically acquired if you want your insurance to be available for such things as long-term care or legacy. Most of my clients need a blend of term and permanent insurance. If you have a few minutes to answer some questions I can help determine the amount and type of life insurance that is appropriate for you.”

Determining the Amount & Type of Life Insurance

Assuming your client is open to assessing their life insurance goals DBS can help. DBS has developed a simple fact finder that not only determines the amount of insurance coverage, but also the type of coverage. To learn more about this and other tools available from DBS contact your dedicated Case Design Analyst.