Multi-Generational Estate Planning for Uninsurable Individuals

THE SITUATION

A financial professional called DBS seeking estate planning advice for a very wealthy widow. The client had previously used most of her estate tax exemption and was still in good health . . . that is for a person 87-years old.

THE PROBLEM

Carriers have a maximum issue age which for most carriers age is 90. Of course, individuals with significant health issues generally cannot qualify for life insurance coverage. The financial representative wanted a “creative idea.”

THE SOLUTION

The call was transferred to DBS’s in-house Advanced Marketing Attorney who suggested that the financial representative might want to have his client consider multi-generational insurance planning.

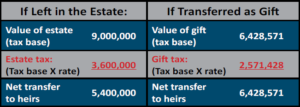

Specifically, the DBS in-house attorney explained that for an individual who has already used their exemption amount, the estate and gift tax rates are both the same at 40%, but a wealthy client can save a significant amount in taxes by making taxable gifts instead of paying estate tax. The following example was provided: (Assume assets available to transfer either by gift or left in the estate equals $9,000,000)

The DBS Marketing Attorney explained that the over $1 million in tax savings could be leveraged by the children of the 91-year-old purchasing insurance.

THE RESULT

The client and her legal advisors loved the idea. The financial representative placed a large life

insurance policy and perhaps more importantly, developed a business relationship with the next generation.